Charting Progress

to 1.5°C through Certification

Interactive Summary

The 2015 Paris Agreement committed signatories to maintaining global average temperatures well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C.

Steel’s status as a fundamental material for the global economy and the significant emissions it produces (10% of global CO2e emissions in 2023) means that getting its decarbonisation journey right is crucial.

The majority of the world’s governments and steel corporations have committed to reducing the sector’s emissions to net zero within the next 26 years.

But how will the steel sector get there?

For the first time, we have drawn a clear connection between what’s required to deliver a 1.5°C-aligned pathway for the global steel sector and ResponsibleSteel’s Decarbonisation Progress Levels.

This new report - Charting Progress to 1.5°C through Certification - demonstrates how ResponsibleSteel certification can drive the change needed for the steel industry to achieve the Paris Agreement.

The results provide a framework for steelmakers and steel users to navigate time-bound certification requirements using the ResponsibleSteel Progress Levels, and for policy makers and financial institutions to incentivise the investments we need to see for the industrial transformation.

Linking Paris-aligned pathways to decarbonisation progress

The ResponsibleSteel Decarbonisation Progress Levels enable like-for-like comparison of all steel sites, globally.

The Progress Levels (PL) provide an internationally consistent framework to measure advancement from PL1, the Basic Threshold (representative of today’s global average), to PL4, Near Zero (the goal for all steelmakers).

The scrap-variable scale incentivises all steelmakers, regardless of their existing technology, location, or scrap availability, to invest in decarbonised production processes. This global perspective to industrial change is critical to ensure a net gain for the climate.

Using two scenarios –the International Energy Agency’s (IEA) Net Zero Emissions (NZE) by 2050, and the Mission Possible Partnership’s (MPP) Carbon Cost (CC) – we link their projections to the ResponsibleSteel Decarbonisation Progress Levels (PLs), allowing us we move beyond technology-led roadmaps to understand how certification can drive the transformation we need to see across the global steel sector.

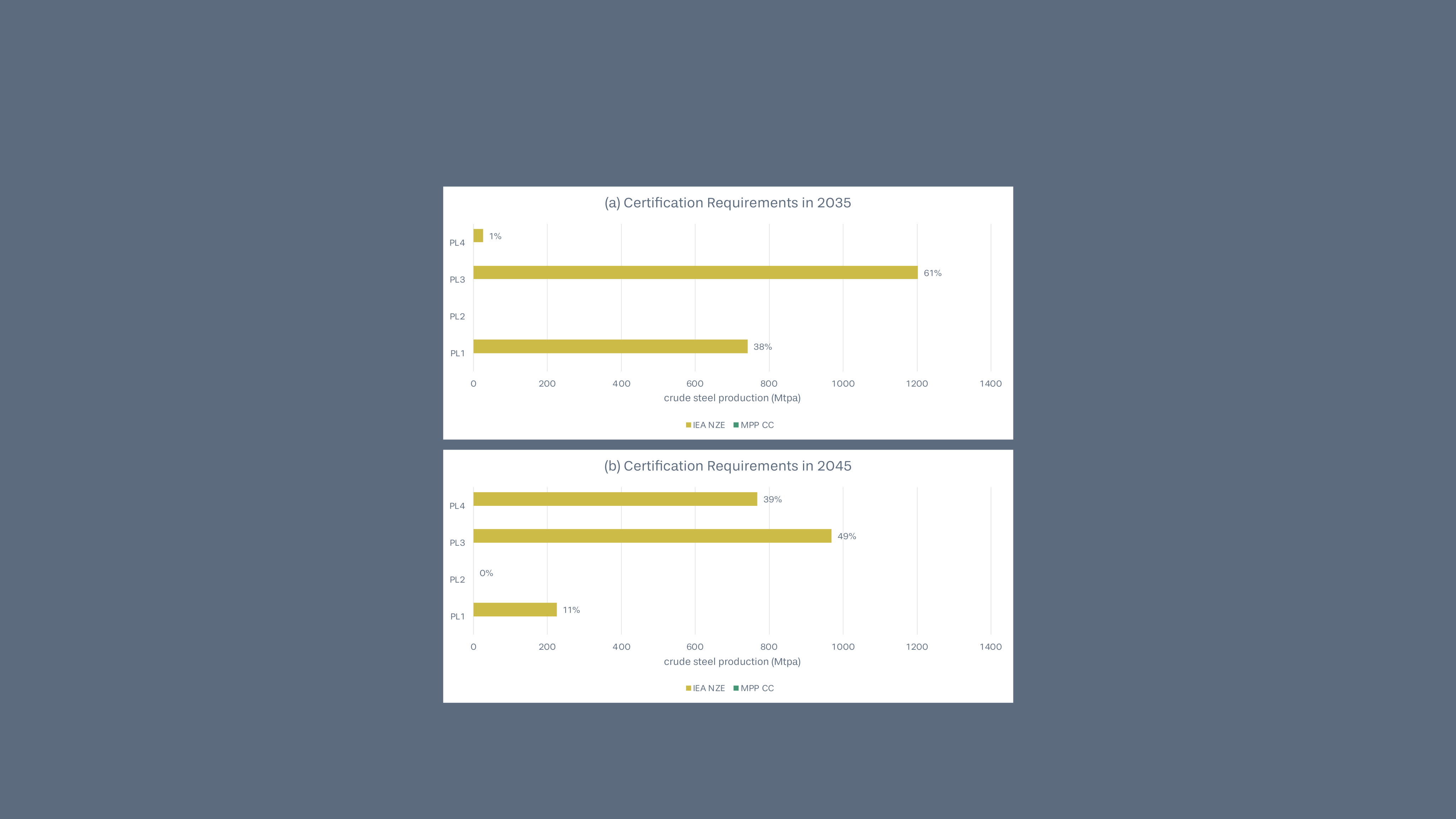

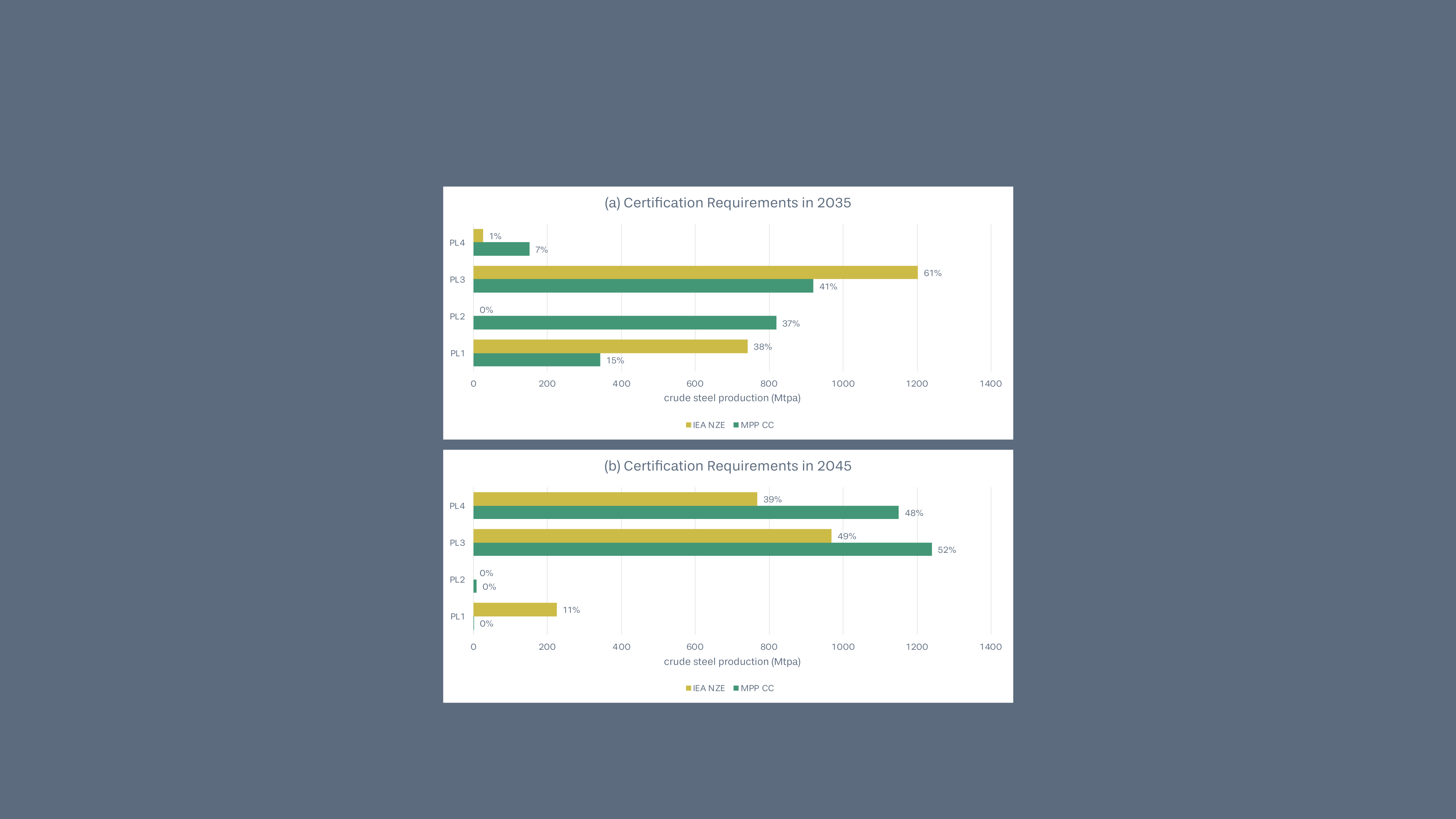

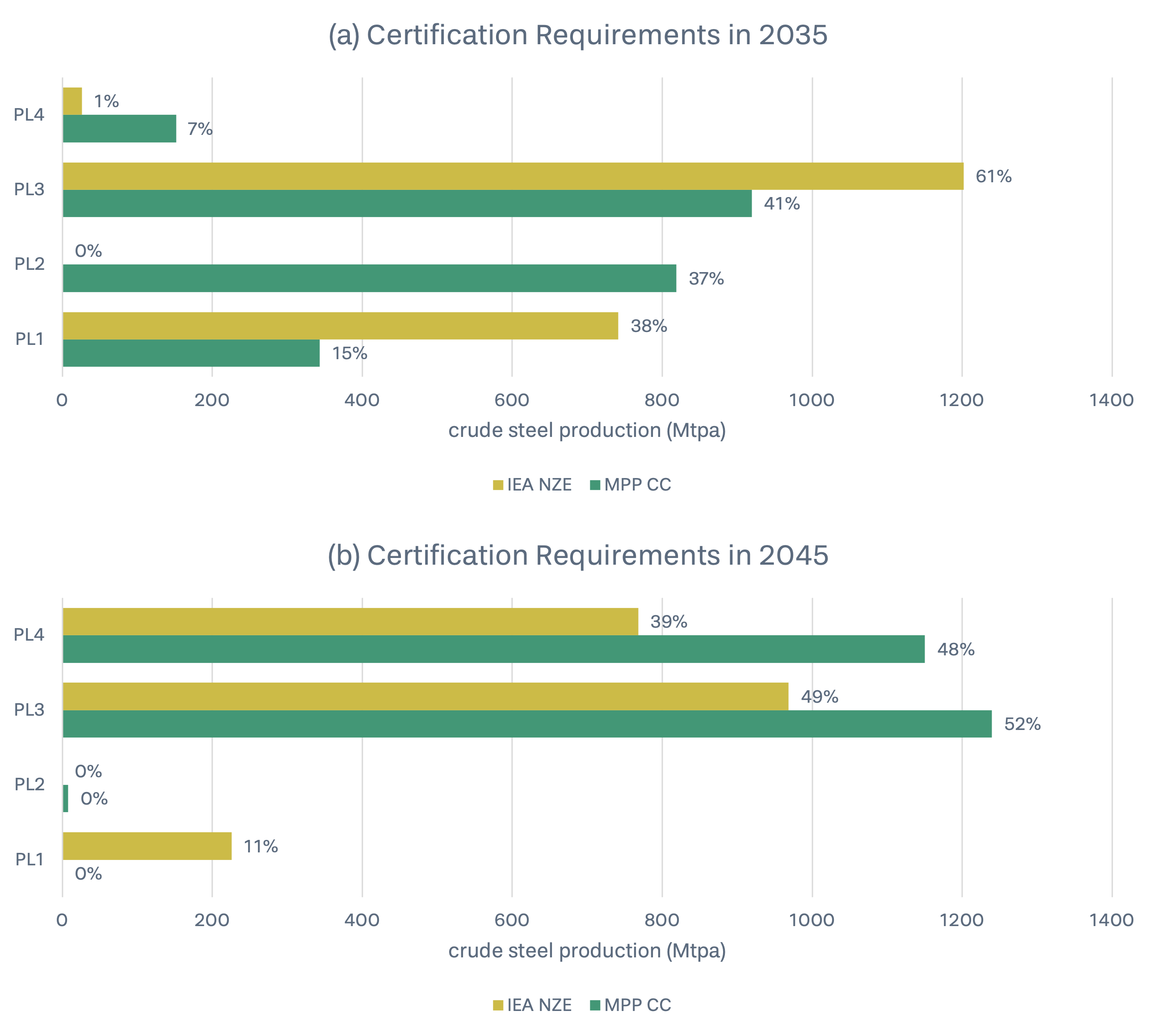

Global ResponsibleSteel certification requirements at key milestones according to the 1.5°C-aligned pathway

Four key findings

1. The entire industry needs to shift but radical change at scale takes time.

The analysis demonstrates the importance of immediate action at scale.

For the steel industry to achieve its Paris Agreement obligations, every steel plant in the world needs to reach the Basic Threshold (Progress Level 1) by 2030, which is equal to or better than today’s average emissions intensity.

In other words, following a 1.5°C trajectory, today’s average steelmaker will become the industry’s worst by 2030 if they don’t improve their operations.

The near-term focus must be simultaneous significant transitional improvements (emission reductions of more than 30% compared to the basic threshold), and breakthroughs (emissions reductions of more than 85% compared to the basic threshold) observed across a leading minority of ‘first movers’

First movers may well be capable of supplying near-zero emissions steel before 2030, however, the overall output and cumulative emissions savings will be minimal to start with.

In Progress Level terms, achievement of a 1.5°C-aligned pathway will require much lower emissions (Progress Level 3) steel production to dominate by 2040, and near-zero emissions (Progress Level 4) by 2050.

It is essential for all steel plants to begin their decarbonisation journey, regardless of their starting point. Progress will not be linear, but must commence immediately.

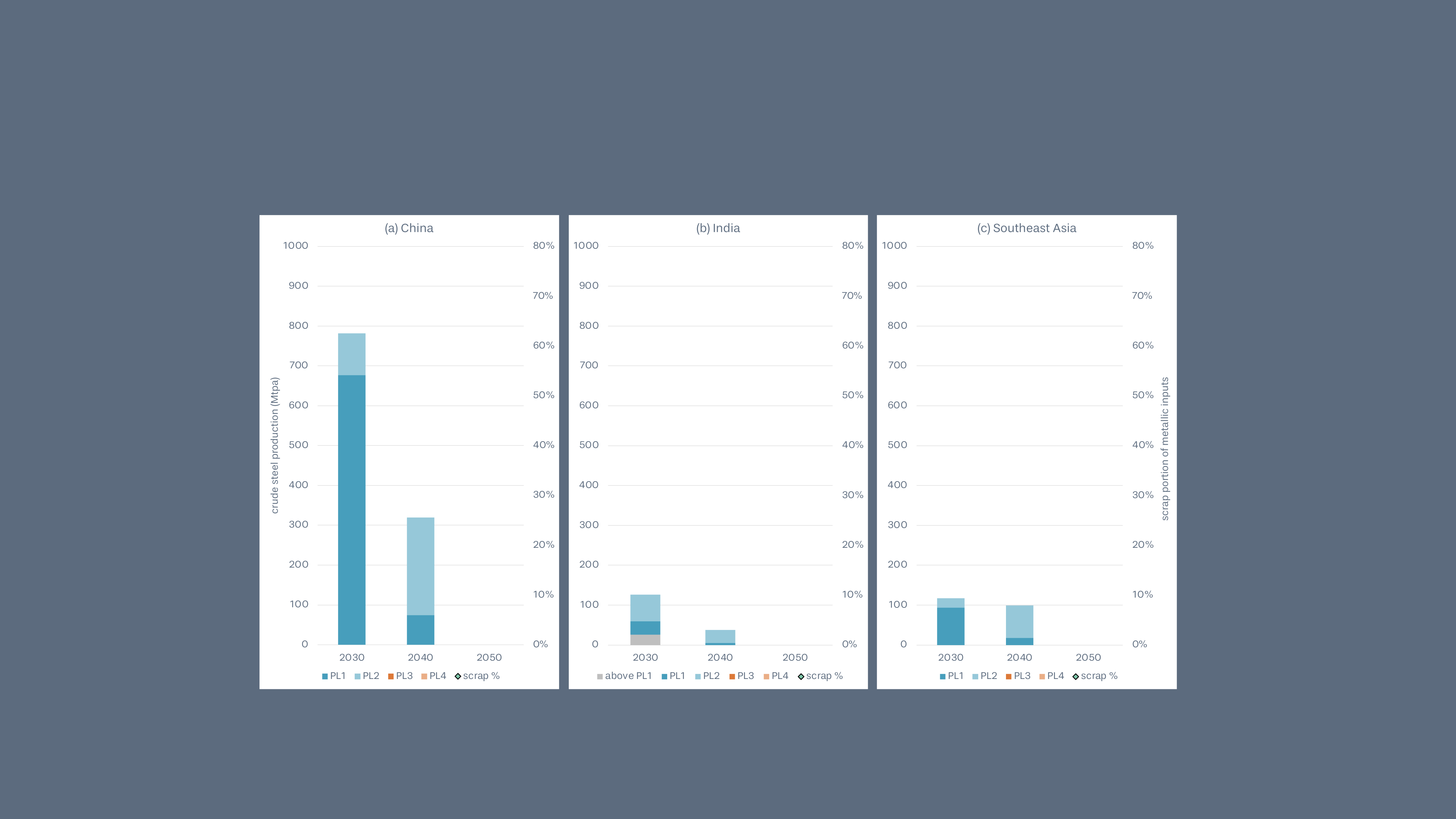

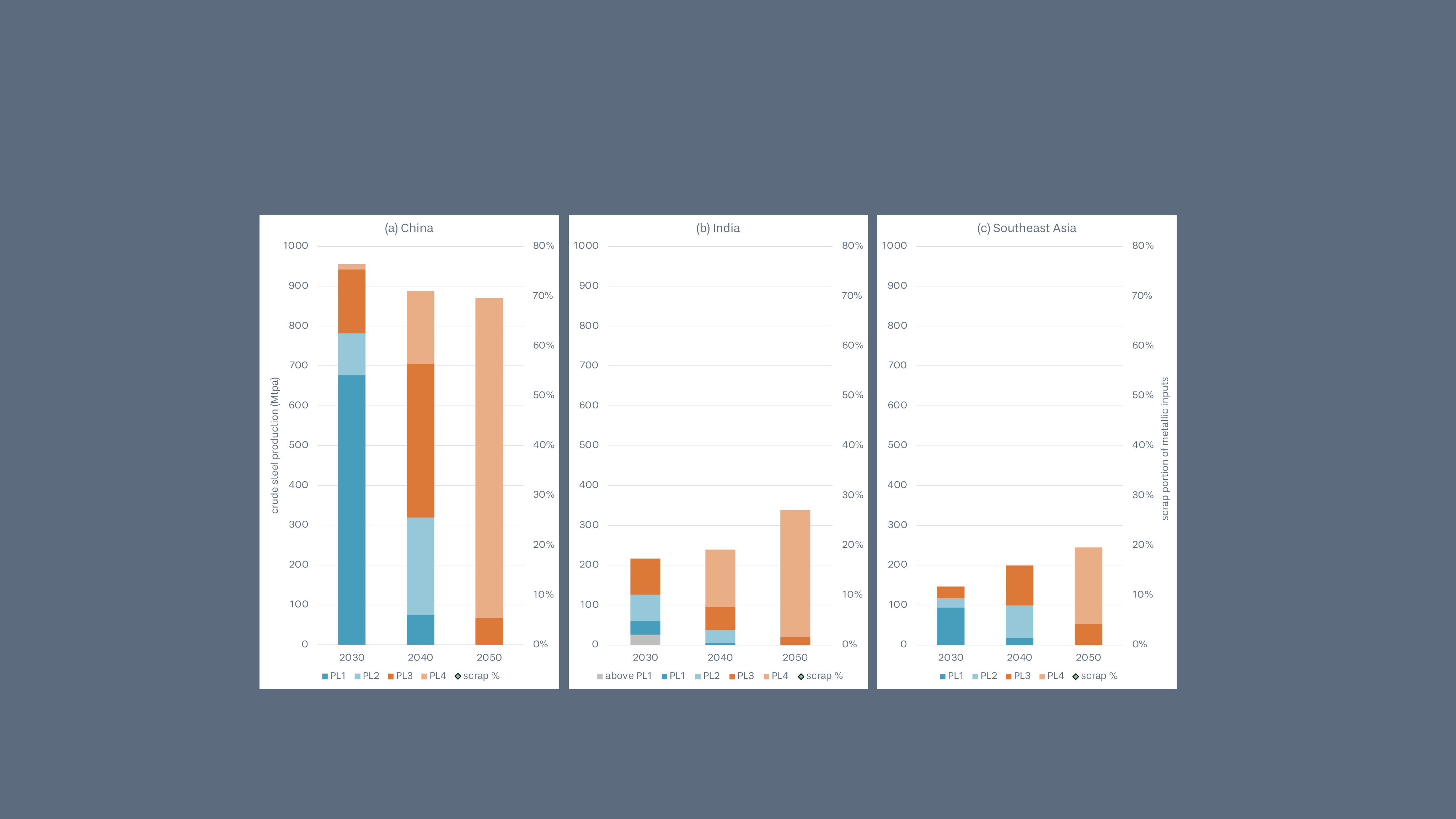

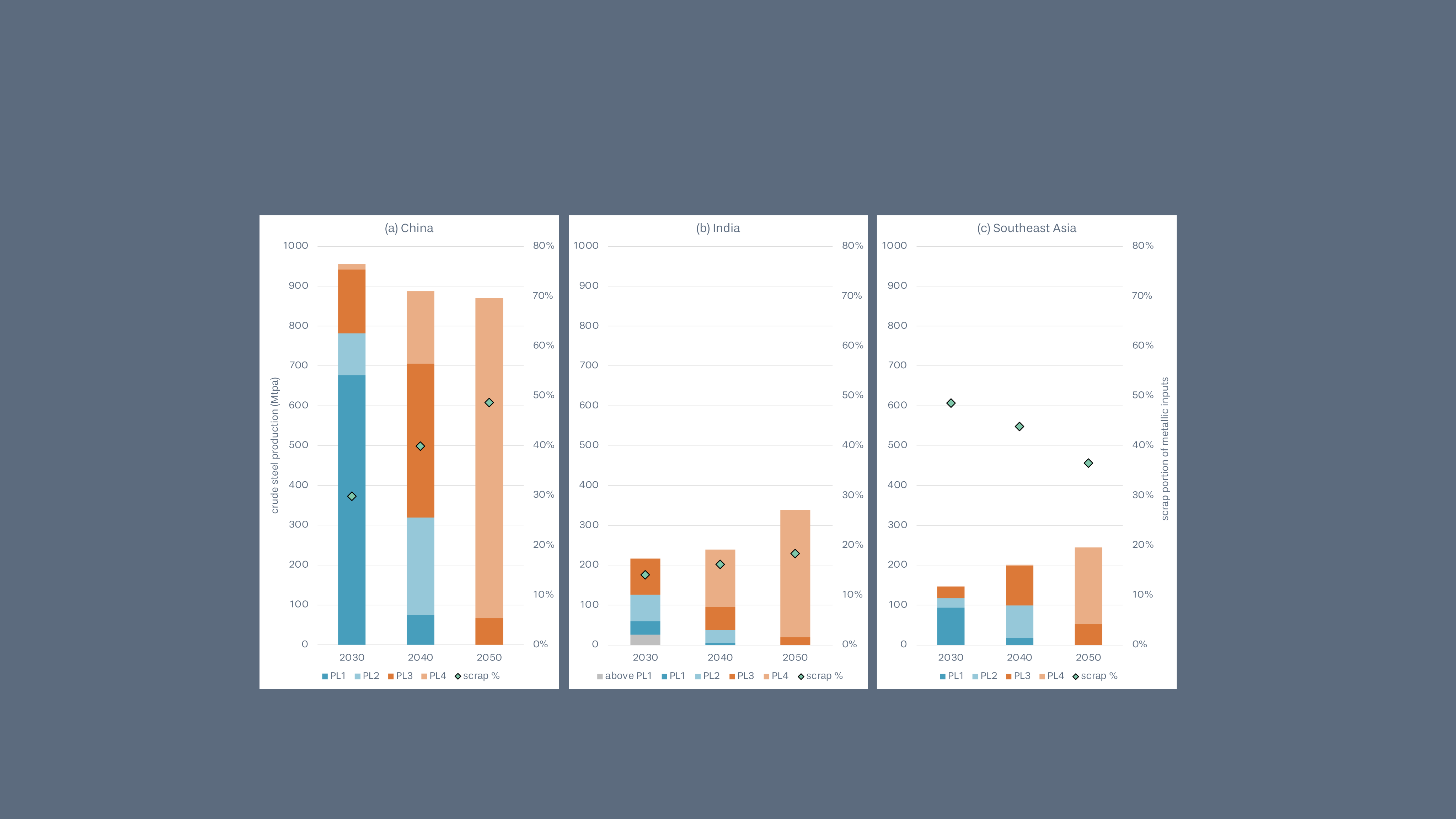

Global 1.5°C-aligned ResponsibleSteel certification pathways from 2020 to 2050

2. Global objectives require regionally nuanced approaches.

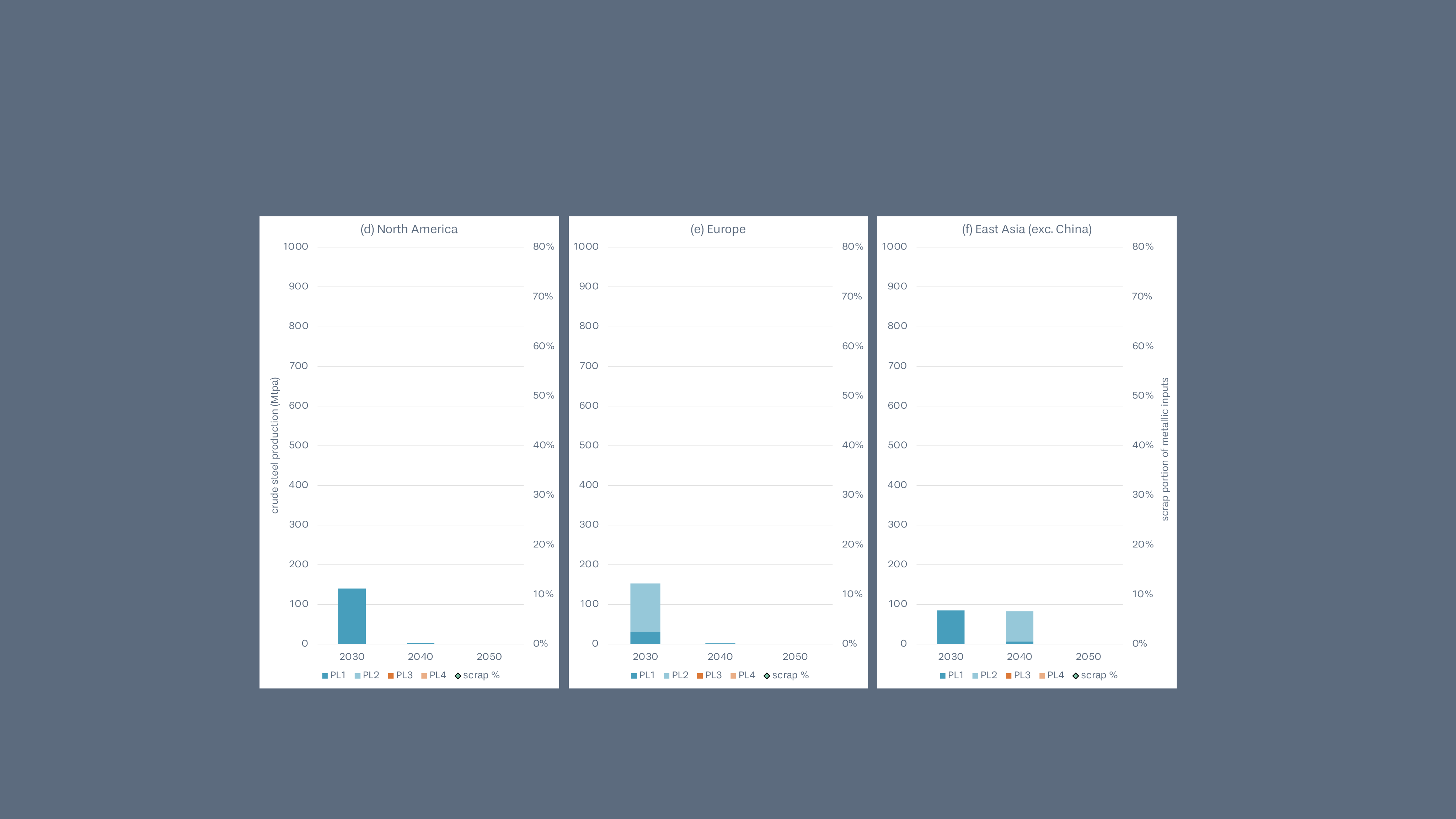

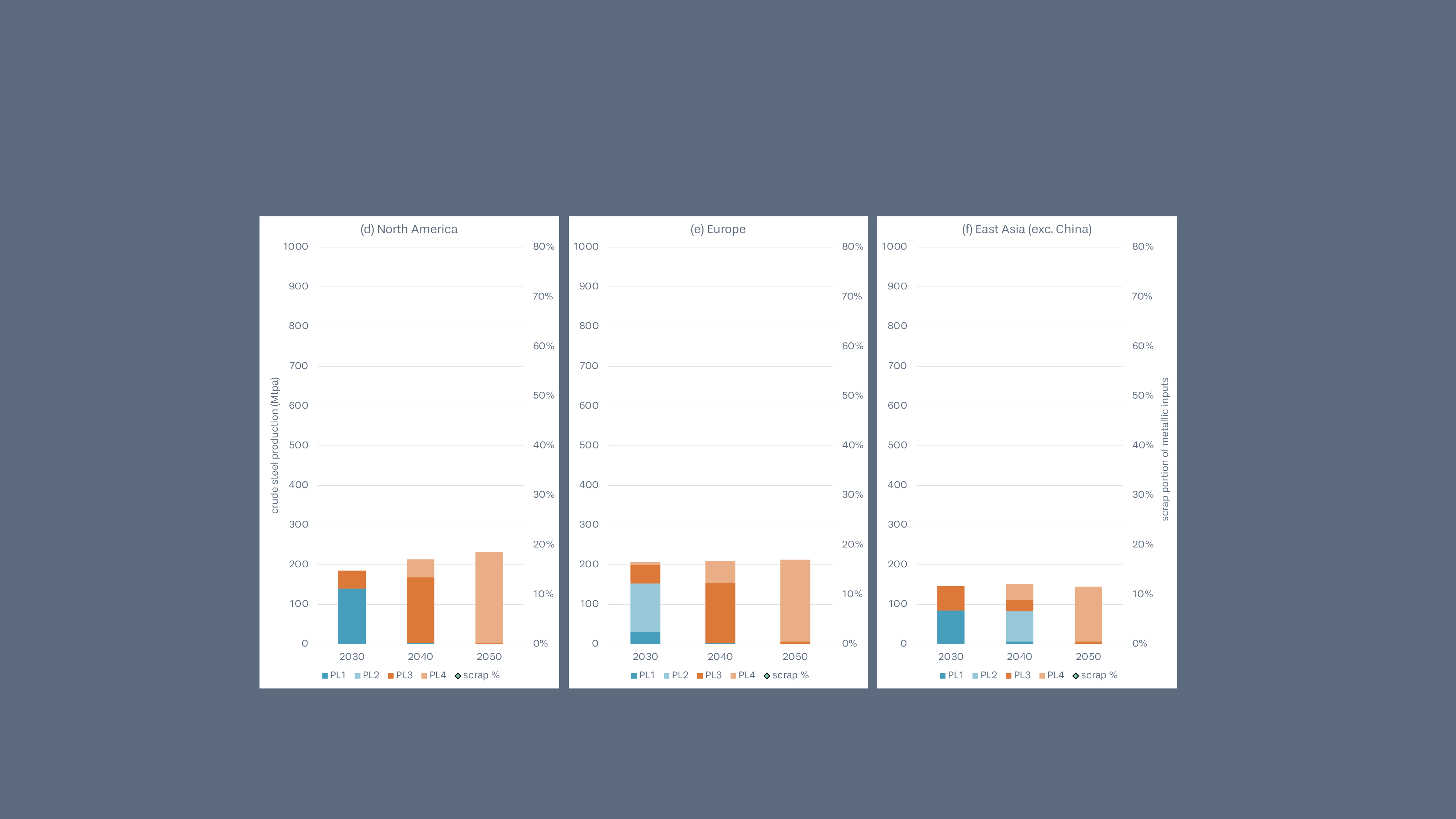

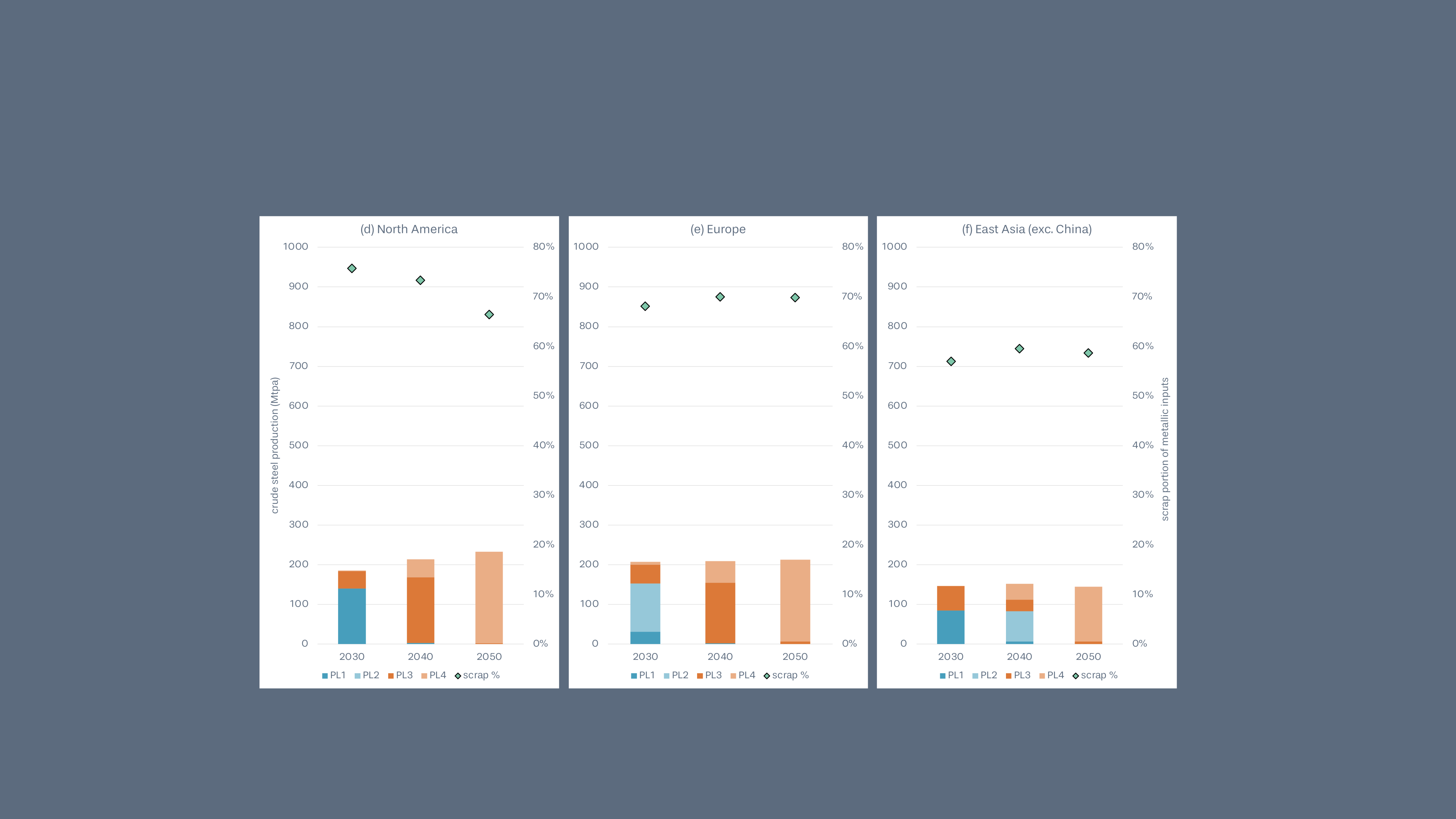

Zooming into six key regions using disaggregated MPP results, certification differences in 2030 are most pronounced. Yet, regions converge towards 2050 as near-zero emissions becomes a fundamental requirement, globally.

The graphs below represent the regional 1.5°C-aligned ResponsibleSteel certification pathways, for (a) China, (b) India, (c) Southeast Asia, (d) North America, (e) Europe and (f) East Asia (exc. China) in descending order of steel production in 2050. Whilst the left-hand vertical axis shows the crude steel production at different Progress Levels, the right-hand vertical axis indicates the scrap inputs to steelmaking (measured as a portion of total metallics).

Across regions, Paris-aligned pathways towards 2050 will be heterogenous, reflected in technology selection, energy mix, and the speed at which near-zero emissions is achieved.

The distinct local conditions affect the direction and speed of industrial change, including existing assets, scrap availability, natural resource endowments, climate policies, and available finance. There is a pathway forward for every single steel plant, and whilst the speed and nature of the transition will be unique, they are not excuses for inaction.

Whilst some regions will follow a steady downward decarbonisation trend, others could leapfrog to near zero.

Accordingly, the ResponsibleSteel International Production Standard allows for unique Paris-aligned pathways by not specifying time-bound targets for Progress Level achievement.

Regions must take charge of their decarbonisation progress, assure ambition, and drive change along a pathway which optimises the local conditions.

3. The reduction of supply chain emissions is critical to reach near-zero.

Upstream indirect emissions related to material and fuel inputs are likely to become a larger share of the total site-level crude steel emissions intensity. Indirect supply chain-related emissions may comprise about one-third of sectoral emissions in 2050, an increase from today’s approximately one-quarter share.

¼ ➔ ⅓

Consequently, steelmakers must engage in intersectoral decarbonisation to simultaneously achieve near zero emissions outside the physical steel site boundary, for example within the iron ore, hydrogen, and ferroalloy sectors.

Emissions distribution graphs for various technology archetypes, in 2030 and 2050, in t CO2e/t

crude steel.

BF-BOF = Blast Furnace-Basic Oxygen Furnace / CCS = Carbon Capture and Storage / DRI = Direct Reduction of Iron / EAF = Electric Arc Furnace / H2 = Hydrogen / MOE = molten oxide electrolysis

Whilst decarbonisation of the power sector is far from certain, the increasingly energy-intensive steel industry can play a powerful role in stimulating demand for near-zero emissions electricity, and/or developing ‘behind-the-meter’ renewable energy projects to directly feed the site.

Decarbonising electricity-related emissions is one of the single most impactful decarbonisation measures for electricity-based ironmaking (e.g. green H2-based direct reduction, direct ore electrolysis) and steelmaking (e.g. EAF operations).

Given investments in, and viable operation of, deep decarbonisation technology (e.g. green H2-based direct reduction, renewables-based ore electrolysis, and carbon capture and storage/utilisation), residual direct emissions cannot be forgotten. To get in reach of near zero, direct emissions from carburising agents, lime fluxes and graphite electrodes must also be minimised.

Industrial decarbonisation requires steelmakers to be accountable both within and beyond the site boundary.

4. Higher steel demand makes the decarbonisation challenge more difficult.

To achieve a net zero industry, the steel sector must reduce the emissions intensity of steel production and/or society must reduce overall steel consumption.

Based on more ambitious assumption of material efficiency and circularity, the IEA NZE scenario assumes steel demand plateauing at 2 billion tonnes towards 2050. This IEA projection is 20% lower than MPP’s modelling of 2.5 billion tonnes of steel demand by 2050.

In the near-term, higher steel demand increases the ambition of certification requirements. Yet, towards 2050, differences in relative certification requirements diminish under the common goal of near-zero emissions. Under demand uncertainty, the steel sector must reduce the emissions intensity of production, as quickly as possible, to near zero.

Global 1.5°C-aligned ResponsibleSteel certification requirements in (a) 2035 and (b) 2045, with direct comparison across the IEA NZE and MPP CC scenarios.

Despite differences in steel demand, the projected global scrap share of metallic inputs to steelmaking is strongly aligned – both IEA and MPP analyses foresee an increase from today’s 35%, to 44-48% by 2050.

This has two key implications for decarbonising steelmaking:

■ scrap flows will increase, so levers must be in place to support expansion of efficient recycling processes to maximise value retention in available end-of-life steel resources, and

■ at least 50% of steel production will rely on iron ore reduction, requiring alternate energy-intensive ironmaking processes.

The ResponsibleSteel Decarbonisation Progress Levels have been strategically developed to drive both enhanced circularity and decarbonised ironmaking, providing an effective framework for industry-wide emissions reductions.

Calls to action

Steelmakers

Get certified now, starting at PL1, then work towards more ambitious Decarbonisation Progress Level achievement. Map your company-level Paris-aligned pathway to 2050 to Progress Levels and use it as a tool to manage climate-related risks, as required by investors and financiers.

Steel buyers

Use your procurement power by sending demand signals for Certified Steel. Look for progress, acknowledging that change takes time, transitional improvements must be rewarded, and near zero emissions will be a long-term outcome for most steelmakers.

Suppliers to steelmakers

Certify lifecycle emissions of your product and understand and demonstrate its contribution to the emissions intensity of steel production. Work towards decarbonisation of your own production through a Paris-aligned pathway to net zero 2050.

Policymakers

Cross-disciplinary policy collaboration - climate, industry, procurement, innovation, trade - will support effective implementation. Use ResponsibleSteel GHG measurement requirements as a common language to compare the embodied emissions of steel needs equitably and globally. Generate the market signals required to stimulate green markets.

Investors & financiers

Regard ResponsibleSteel Certification as a framework of common indicators for sustainability performance and disclosure across steel companies in your portfolio on climate and ESG. Ask to see Core Site Certification to ensure your broad sustainability goals are covered and ask for Steel Certification to enable you to compare the progress of different stocks towards near zero on a like-for-like basis.

Civil society organisations

Mandate change across the steel value chain using the language of Decarbonisation Progress Levels. Encourage investors to value ResponsibleSteel Certification as good practice across their steel portfolio. Influence steel consumers to procure ResponsibleSteel Certified Steel at more ambitious Progress Levels over time.

Industry bodies

Encourage ResponsibleSteel Certification among your members and map the collective pathway for combined membership through the lens of Decarbonisation Progress Levels.

ResponsibleSteel Members

Join our upcoming working group to develop the approach to science-based target setting and Paris-aligned pathways (Criterion 10.1). We will build on findings from this Report to ensure an equitable and practical decarbonisation framework.

Ambition and urgency are required to ensure commitments made under the Paris Agreement are achieved.

Industrial decarbonisation of the steel sector will not be easy, but it must be done.

In the 26 years from 2024 to 2050, business-as-usual must move from the Basic Threshold (Progress Level 1) to Near Zero (Progress Level 4). To do so, an effective credible global standard and certification scheme will be instrumental in:

■ Establishing and maintaining equitable guardrails for achieving sustainable steel production;

■ Providing a lens through which the entire steel value chain can measure and verify decarbonisation progress consistently;

■ Enabling lower/much lower/near-zero emissions steel markets to flourish.

The ResponsibleSteel International Production Standard is ideally positioned as a powerful tool for steelmakers, policymakers, financial institutions, trade organisations, and campaigners, to support genuine decarbonisation of the steel sector at large.